AI-free as a Promise of Quality?

Context

Generative AI has moved from back-office data tool to front-facing creative engine. Industry leaders like Coca-Cola and Burger King now produce campaigns using AI-generated imagery and copy, while a growing counter-movement of brands publicly commits to human-only creative production. At the same time, consumer trust in AI is far from settled — surveys indicate that while half of US adults use generative AI tools, a large share distrusts how brands deploy them, and a social stigma around AI use is emerging.

This tension raises a consequential strategic question that has received almost no empirical attention: does publicly positioning a brand as AI-free or AI-first produce measurable differences in how consumers evaluate it — and if so, why?

Goal and Research Questions

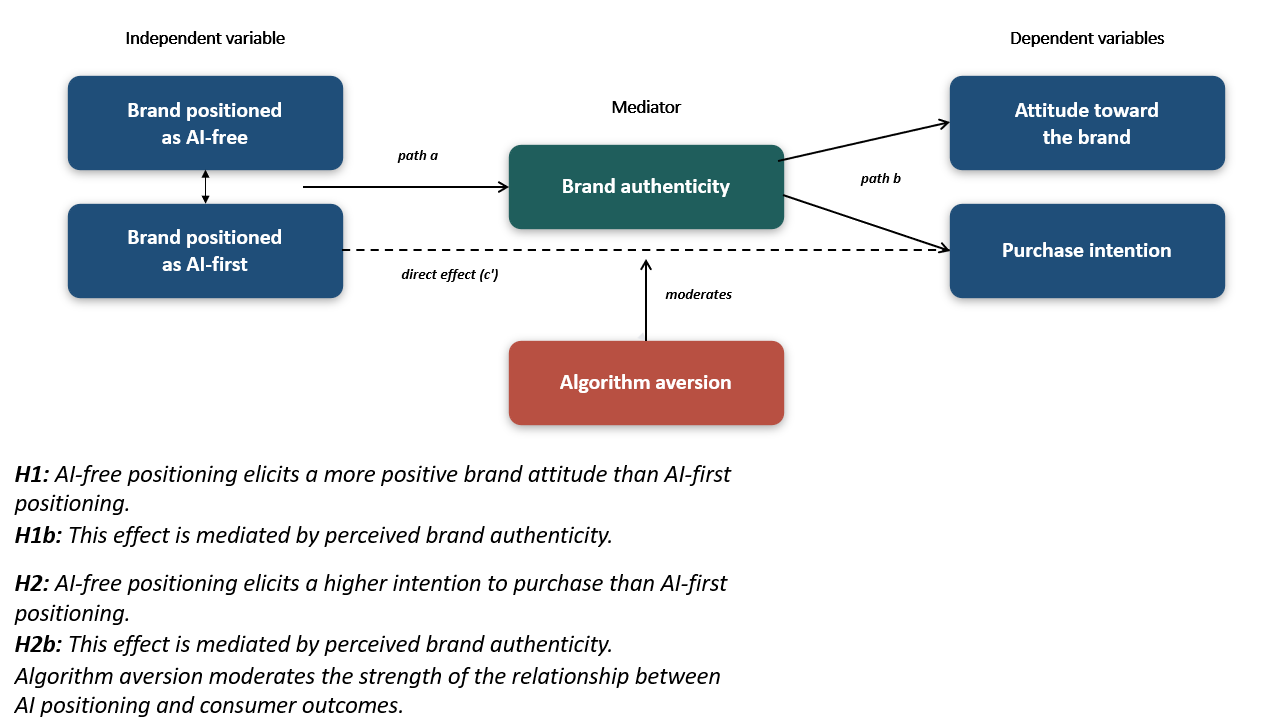

The study set out to answer two hierarchically related research questions:

- Does an explicit AI-free brand positioning, relative to AI-first positioning, produce more favourable consumer attitudes and higher purchase intention?

- Does brand authenticity mediate this relationship — and does algorithm aversion moderate its strength?

A fictitious sunglasses brand, Roy Sunglasses, was used as the experimental stimulus. This ensured that any differences in consumer response could be attributed to positioning alone, uncontaminated by existing brand equity or product familiarity.

Methods

The study used a between-subjects experimental design administered via Qualtrics. Participants were randomly assigned to one of two conditions:

- Condition A (AI-free): Roy Sunglasses commits entirely to human creative production — no AI in design, campaigns, or copy.

- Condition B (AI-first): Roy Sunglasses declares generative AI as its primary creative tool — all images, campaigns, and copy are AI-generated.

Both stimuli were written as first-person brand manifestos, equal in length and structure, differing only in their stance toward AI.

A total of 138 valid responses were retained after quality filtering (out of 160 collected), split near-evenly between conditions. The sample spanned 17 countries, with the largest contingents in Switzerland (51%) and Brazil (17%), and skewed toward 18–24 year-olds and frequent AI users.

Analytical tools included:

- Independent samples t-tests for the main effects (H1, H2)

- Bootstrapped mediation analysis via Hayes' PROCESS macro Model 4 (H1b, H2b) with 5,000 resamples

- Moderation analysis via PROCESS Model 1 with Johnson-Neyman probing

- Exploratory willingness-to-pay analysis (chi-square and Mann-Whitney U tests)

- Robustness checks with psychographic and demographic covariates

Constructs measured included brand attitude (affective + cognitive), purchase intention, perceived brand authenticity (heritage, sincerity, quality), and algorithm aversion.

Results

Main effects were large and unambiguous.

AI-free respondents formed significantly more positive brand attitudes (M = 5.29) than AI-first respondents (M = 3.61), with a very large effect size (d = 1.39, p < .001). Purchase intention followed the same pattern (M = 4.31 vs. 2.72, d = 1.14, p < .001) — with the AI-first mean falling below the scale midpoint, indicating active disincline rather than mere indifference.

Brand authenticity fully mediated both effects.

Authenticity accounted for approximately 81.5% of the total effect on brand attitude and 82.7% on purchase intention. Once authenticity was included as a mediator, the direct effect of positioning became non-significant in both models. AI-free positioning is not producing a general "warm feeling" — it is specifically restoring a perception of authenticity that AI-first positioning destroys.

Algorithm aversion amplified the effects — especially for purchase intention.

Among consumers with high algorithm aversion (78–87% of the sample), the AI-free advantage on purchase intention was very large. At low algorithm aversion, the AI-free advantage on attitude remained significant but disappeared entirely for purchase intention — suggesting aversion is a stronger gatekeeper of spending decisions than of attitude formation.

Willingness-to-pay told a concrete commercial story.

Only 28% of AI-first respondents said they would buy Roy Sunglasses at a USD 100 anchor, compared to 61% in the AI-free condition. Mean maximum WTP: $72.70 (AI-first) vs. $113.34 (AI-free) — a gap of $40.64, or 55.9% (p = .002).

The central interpretive reframe:

The data suggest the gap between conditions is better understood as an AI-first penalty than an AI-free premium. AI-free positioning lands modestly above neutral reference points; AI-first positioning falls well below them. AI-free preserves a baseline of favourable evaluation that consumers extend to brands by default in craft-relevant categories. AI-first destroys it.