Decoding ESG in financial materiality, rating divergence, and comparability across industries

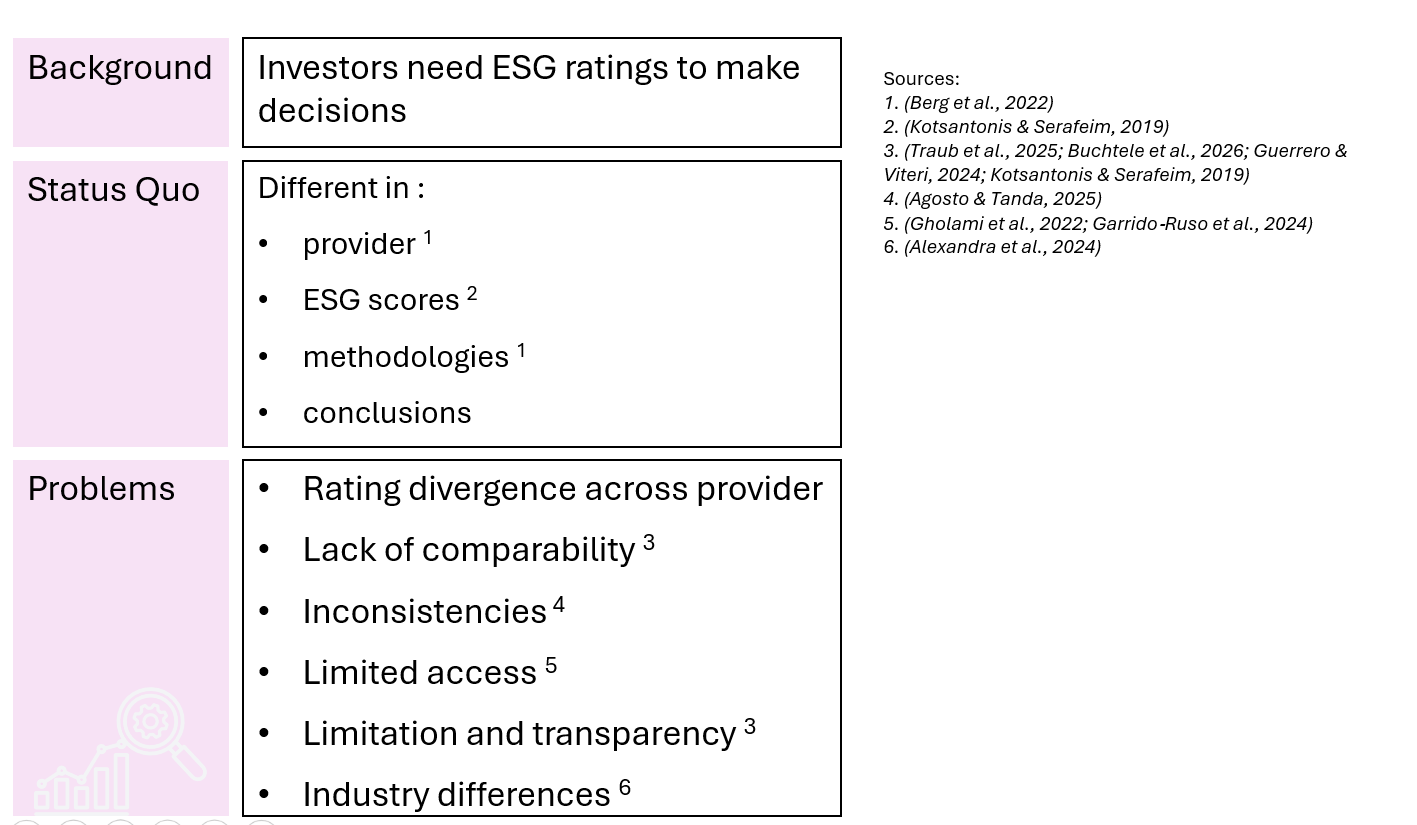

Nowadays, ESG factors have become more important due to growing consumer demand for sustainable products, stricter regulations, and the increasing integration of ESG information into investment decisions because investors use ESG ratings to evaluate sustainability-related risks and identify long-term opportunities.

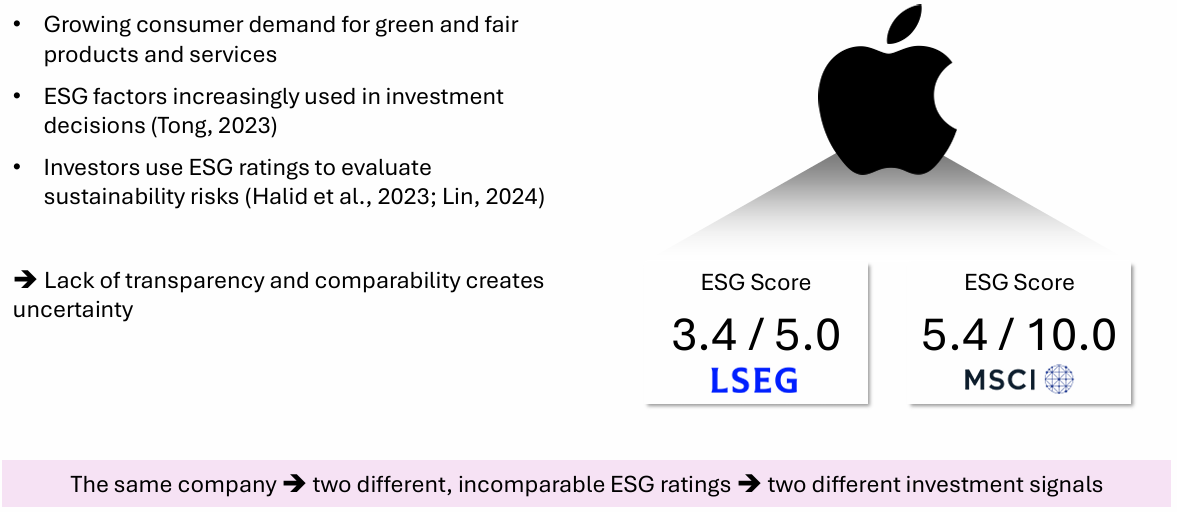

Imagine that two investors want to invest in Apple. They are analyzing exactly the same company, but they use different ESG providers. Surprisingly, they receive different ESG scores. So, from this example, it's showing lack of consistency and comparability and also lack of transparency in ESG ratings that creates uncertainty for investors.

Problem statement

As mentioned, investors rely more on ESG scores. However, different providers often apply different methodologies and weighting systems. As a result, the same company can receive different ESG scores and potentially send different investment signals.

This creates several challenges, including rating divergence, lack of comparability, inconsistencies, limitations and transparency, limited access, and industry differences to compare.

Therefore, investors may find it difficult to know which ESG information they should rely on.

Research question

Research Objective

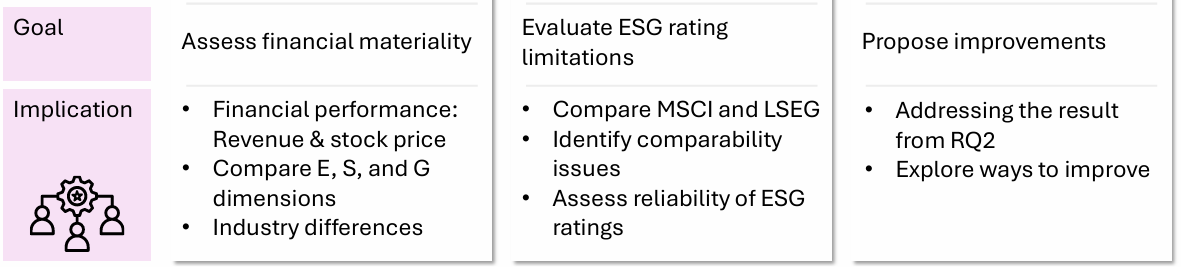

Based on the challenges, this study is structured with three sub-research questions

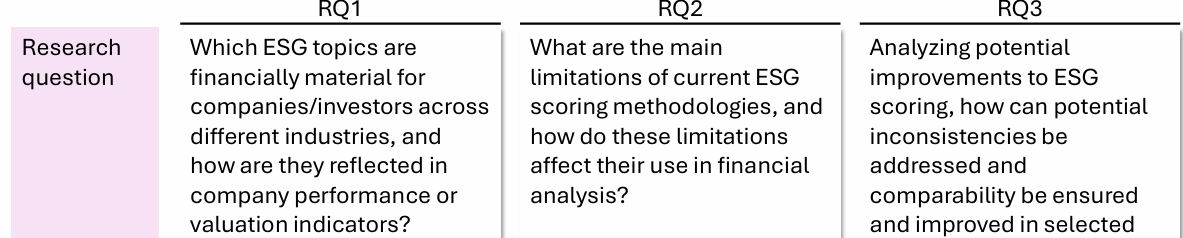

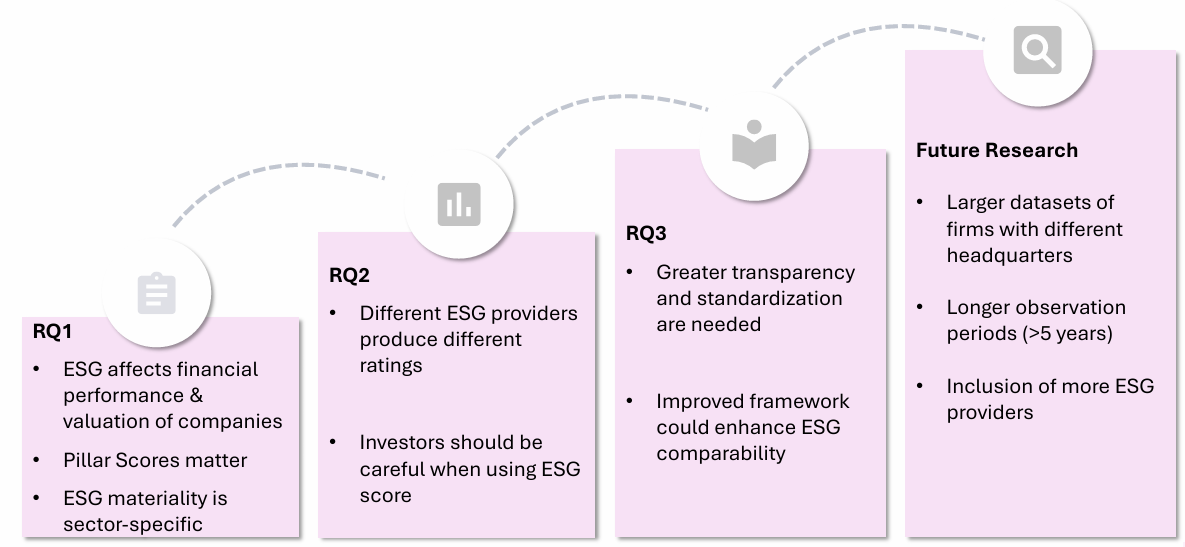

RQ1 examines the financial materiality of ESG by analyzing how ESG factors affect financial performance. And which ESG topic are most impact across different industries.

RQ2 investigates ESG rating divergence by comparing differ provider and identifying issues related to comparability and reliability.

RQ3 builds on these findings and proposes possible improvements to enhance ESG scoring and comparability.

Methodologie

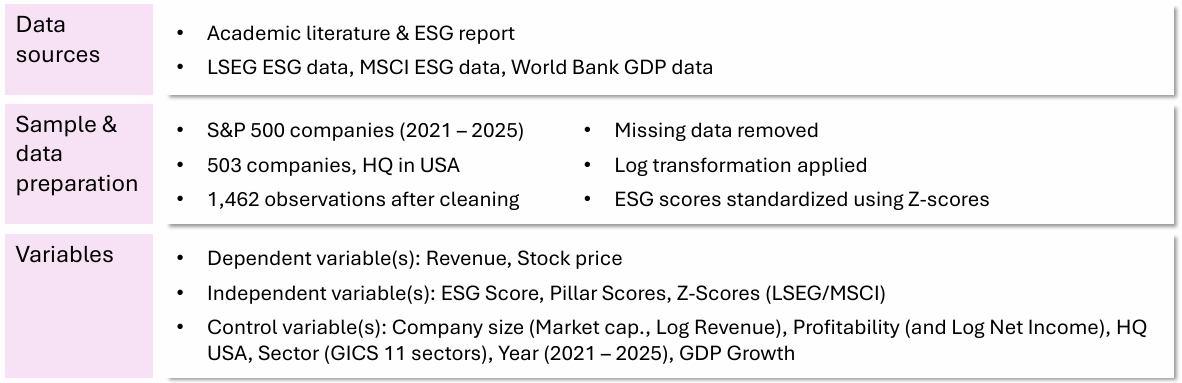

To answer the research questions, a mixed-method approach was adopted, combining quantitative analysis using ESG datasets from LSEG and MSCI, World Bank GDP data was included as a macroeconomic control variable. Supporting qualitative analysis mainly relies on secondary data, including academic literature and ESG reports.

- Sample and preparation: used S&P 500 companies between 2021 and 2025. The initial sample consisted of 503 companies, and after data cleaning, the final dataset contained 1,462 observations.

- Applying logarithmic transformations and standardizing ESG scores by using z-scores between LSEG and MSCI.

- Preprocessing steps were collecting data, removing missing data, applying logarithmic transformations, and standardizing ESG scores by using z-scores between LSEG and MSCI.

- Dependent variable: Revenue and Stock price

- Independent variable: included with ESG scores, ESG pillar scores

- Control variables: including company size as market capitalization, profitability as net income, sector, HQ, and year.

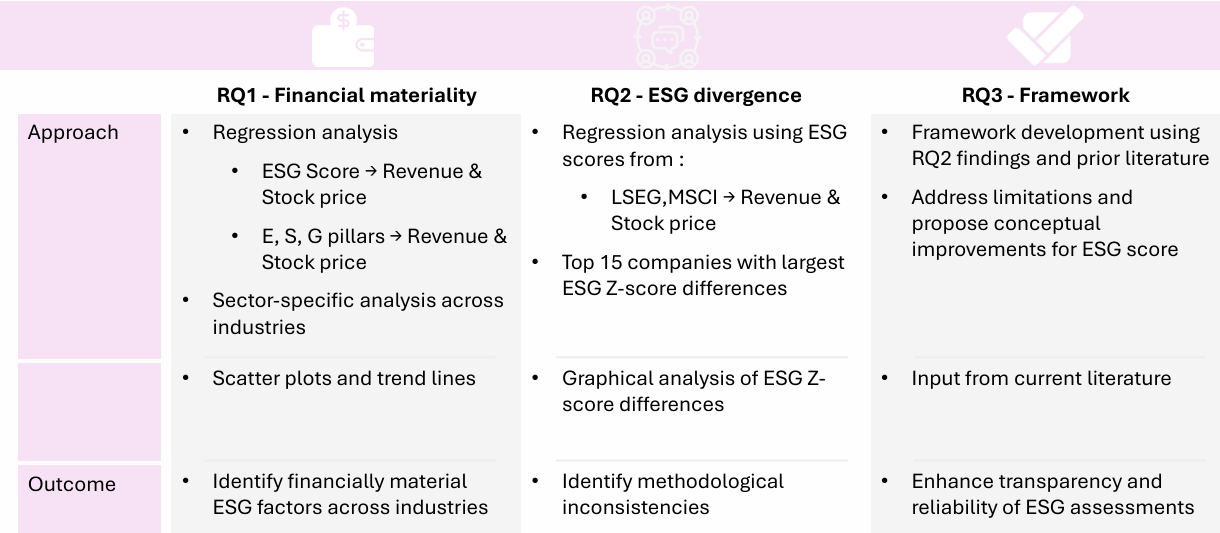

After preparing the dataset. With the first 2 questions by using R Studio. And both RQ 1 and 2 results were supported by scatter plots.

RQ1, used regression analysis to examine the relationship between ESG performance and financial performance in revenue and stock price. Included both the overall ESG score and the ESG pillar scores, together with sector-specific analysis across industries.

RQ2, compare ESG scores from LSEG and MSCI using the regression analysis for comparison. And creating the top of 15 companies with different scores and support by graphical analysis.

RQ3, built on the findings from RQ2, assesses issues and discusses possible improvements to current ESG scoring approaches.

Result RQ1 (1/3)

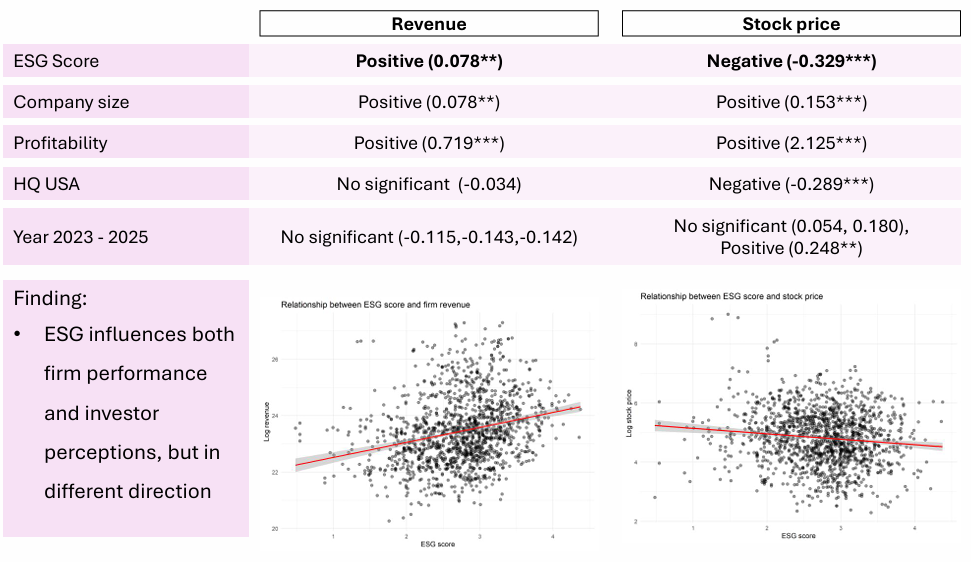

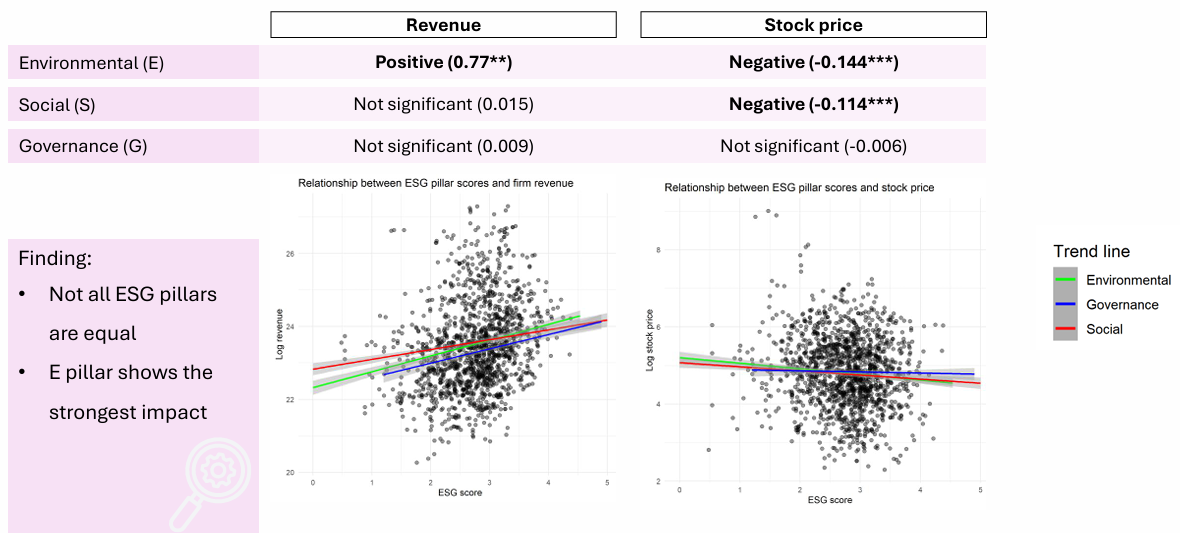

Moving to the first research question, starting with the overall ESG score, the results show two interesting findings.

- First, ESG performance has a positive impact on revenue. Suggests that companies with stronger ESG practices tend to generate higher revenues, possibly due to stronger stakeholder trust and operational benefits.

- However, the relationship with stock price is negative. This indicates that investors may perceive ESG activities as additional costs , they may have to heavily invest on ESG activities, no profit in the short term but rather in long term, which can negatively affect market valuation.

Overall, these findings suggest that the impact of ESG performance on financial performance and investor perception may vary.

Result RQ1 (2/3)

When breaking ESG into its individual dimensions…

- E pillar performance has a positive and significant relationship with revenue but, but a negative relationship with stock price.

- S pillar showed no significant effect on revenue but a negative effect on stock price.

- G pillar was not significant for either revenue or stock price.

Overall, the results suggest that not all ESG dimensions are equally important. So, among the three pillars, environmental factors appear to be the most financially material.

Result RQ1 (3/3)

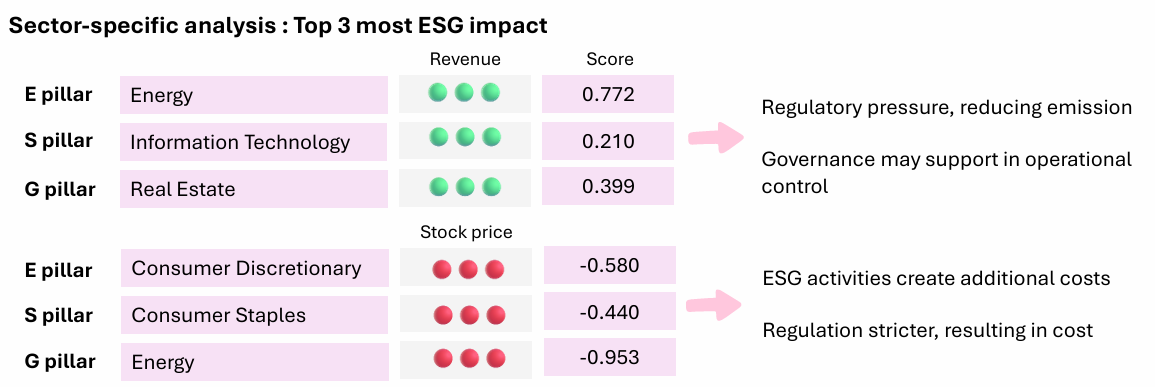

I also analyze the Sector-specific with the regressions. And I selected the top three sectors with the strongest ESG pillars impacts.

First, looking at revenue, all three ESG pillars show a positive and significant effect.

- The Environmental score has positive impact in the Energy sector.

- The Social score has positive impact in Information Technology.

- The Governance score positive impact in Real Estate.

Possible reasons based on the literature with highly polluting industries such as Energy face stronger regulatory pressure, so reducing emissions and improving environmental practices may enhance financial performance. Similarly, governance quality may support revenue generation in sectors where operational control like Real Estate.

However, when we look at stock prices, we find the opposite result.

- Environmental score has negative impact in Consumer Discretionary.

- Social score has negative impact in Consumer Staples.

- Governance performance negative impact in the Energy sector.

This may indicate that investors perceive ESG initiatives as additional costs. Plus for the governance structure are not flexibility, with stricture regulation, more cost in operational, which can reduce expected returns and negatively affect stock valuations

Base on the result : these findings show that ESG pillar effects are sector-specific rather than universal, and different industries are influenced by different ESG dimensions.

Result RQ2 (1/2)

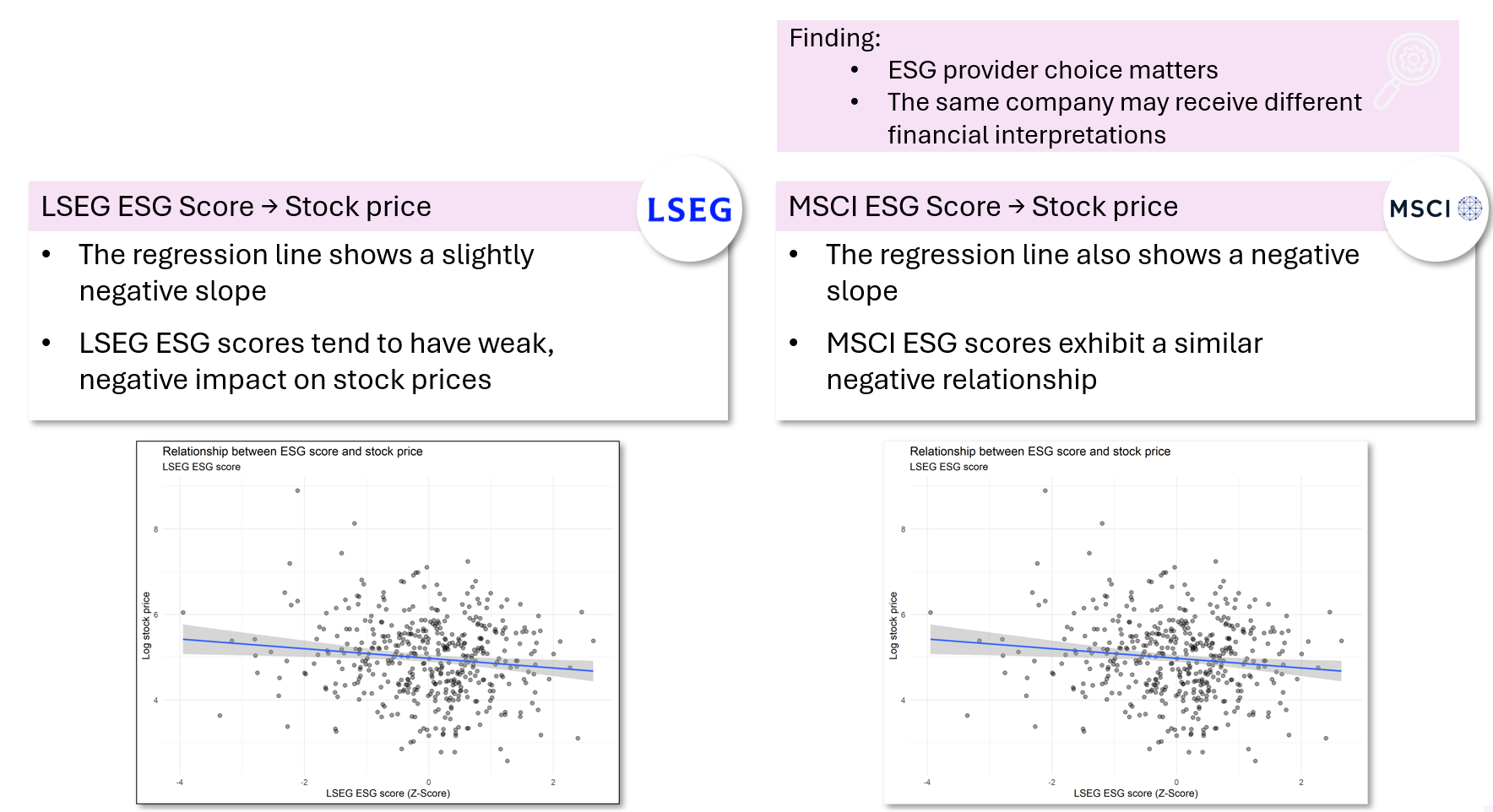

The second research question focuses on ESG rating divergence between LSEG and MSCI providers.

Using the same sample and the same regression analysis, compare whether ESG scores from different providers produce similar or different in financial interpretations.

For revenue, LSEG shows a positive relationship between ESG performance and revenue, whereas MSCI shows a weaker and slightly negative relationship.

For stock price, both providers indicate a negative relationship but still difference score

These findings suggest that the same company can receive different financial interpretations depending on which ESG provider is used.

Results RQ2 (2/2)

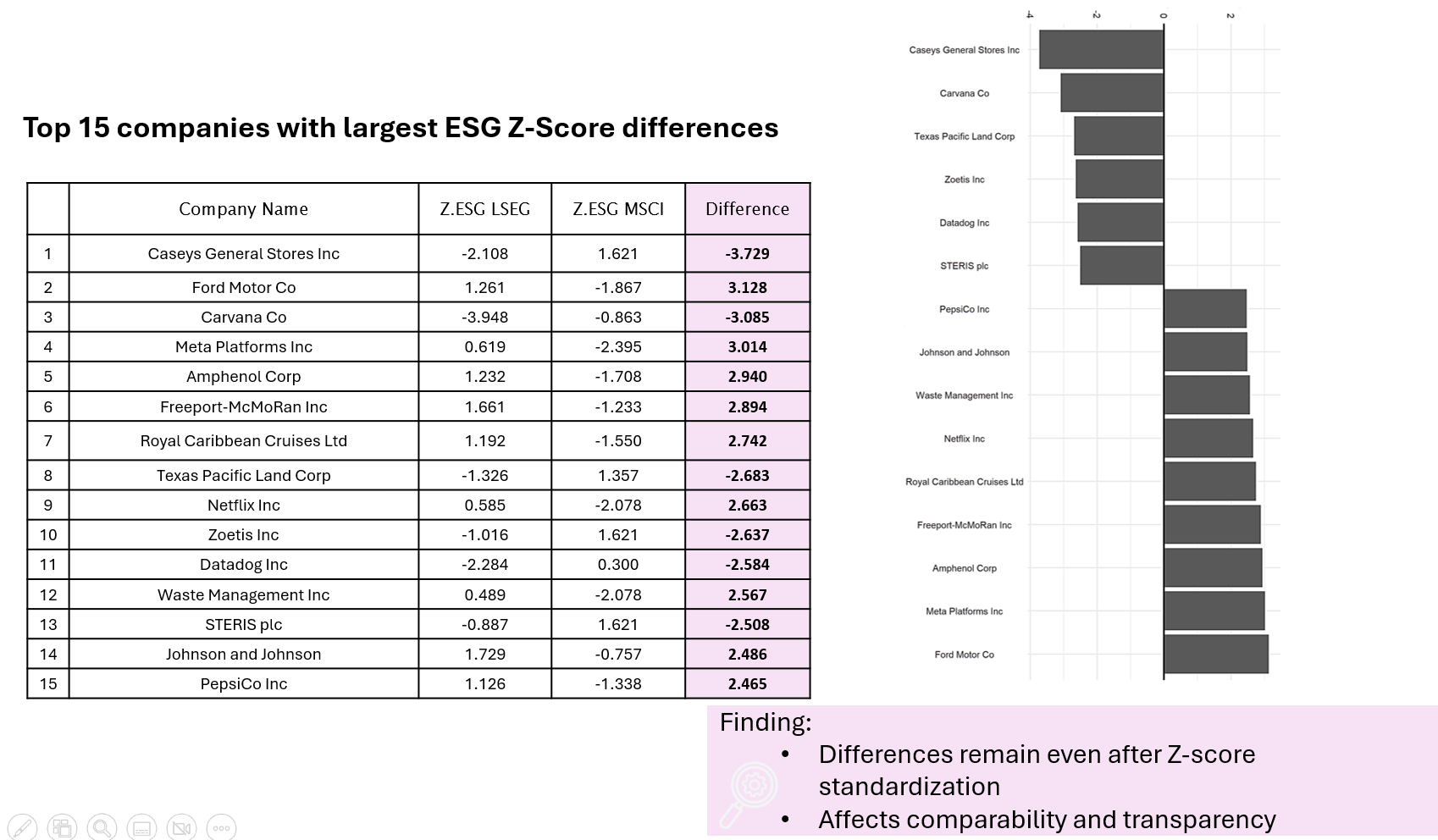

Supporting with The 15 companies with the largest differences between LSEG and MSCI.

The results show different ESG score numbers across providers, even using Z-scores for comparison.

Overall, the findings confirm that ESG divergence is not only a theoretical issue, but also a practical challenge that can affect comparability, transparency, and investment decisions.

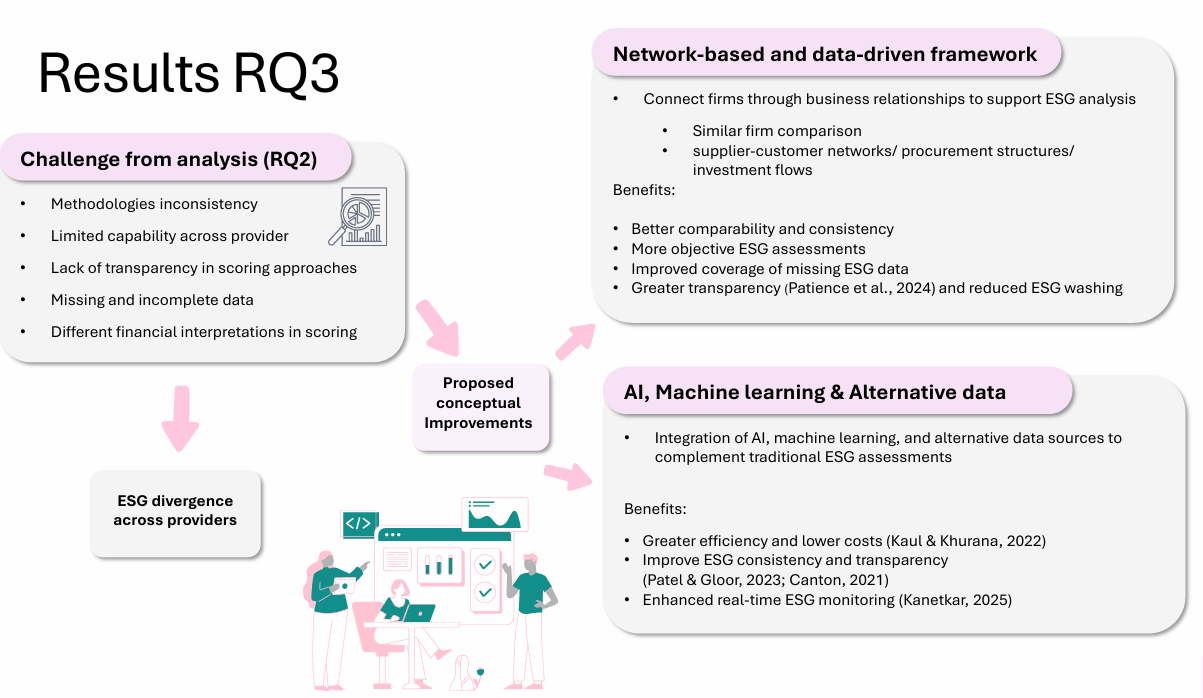

Results RQ3

The third research question focuses on how ESG comparability, transparency, limitations, and inconsistency can be improved.

Based on the challenges identified in RQ2. I proposed two main conceptual improvements.

- The first is a network-based and data-driven framework. This approach connects firms through business relationship connections, such as supplier-customer networks, procurement structures, and investment flows. Since companies with similar operational structures are likely to face similar ESG exposures, this framework could improve comparability, same standard ESG, support more objective assessments, reduce information gaps, and increase transparency.

- The second improvement is the integration of AI, machine learning, and alternative data sources. These technologies could complement traditional ESG assessments by enabling more efficient analysis, improving consistency and transparency, and supporting real-time ESG monitoring.

Discussion and conclusion

Overall, this study shows that ESG factors are financially relevant, as ESG performance can influence both financial performance and valuation.

However, the importance of ESG differs across industries, suggesting that ESG is not a universal concept and that companies should focus on the issues that are most material to their sector.

The study also highlights that investors should not rely on a single ESG rating, as different providers may assess the same company differently. Therefore, improving transparency and comparability is important to make ESG information more reliable and support better investment decisions.

For future research, I would collect larger datasets with firms from different headquarters, longer time periods, and several ESG providers that could help the reliability of the results.