Financial impact of early retirement

Research topic and relevance

Early retirement is a topic that concerns many people in Switzerland, as a large proportion of the population would like to retire earlier. The main reasons for this are that they want to enjoy their retirement for longer and spend more time with their families or pursuing their hobbies.

What many people underestimate is the cost of early retirement. On the one hand, income from employment is lost earlier, and on the other hand, pension benefits are reduced. In addition, there are many unforeseeable risks such as inflation or high healthcare costs. If people have no assets in old age, the state, i.e. the Swiss population, has to pay for it. The Swiss pension system is already struggling with challenges such as longer life expectancy and low birth rates. This means that fewer people are paying into the system, but more pensions have to be financed. Furthermore, pensions tend to be paid out for longer than planned. As a result, the Swiss pension system does not have the capacity to provide financial support to early retirees later on.

Objectives

The aim of the bachelor thesis is to analyse the financial implications of early retirement for an average Swiss person. The impact on income, financial situation, taxes and pension assets will be examined. The thesis should highlight the conditions under which early retirement is viable, the risks that must be taken into account and where there is room for optimisation. Ultimately, it should provide prospective pensioners with an overview of the changes they can expect and help them make a decision.

Methodical approach

A secondary data analysis with a scenario-based approach was used for the investigations. This means that existing data was used, entered into a financial plan and finally compared in various scenarios.

Existing data was used because it had already been collected by the Federal Statistical Office and a separate survey would not have covered the entire Swiss population. A financial plan was drawn up to illustrate the complex financial influences. This made it easy to compare the scenarios and highlight the most important points.

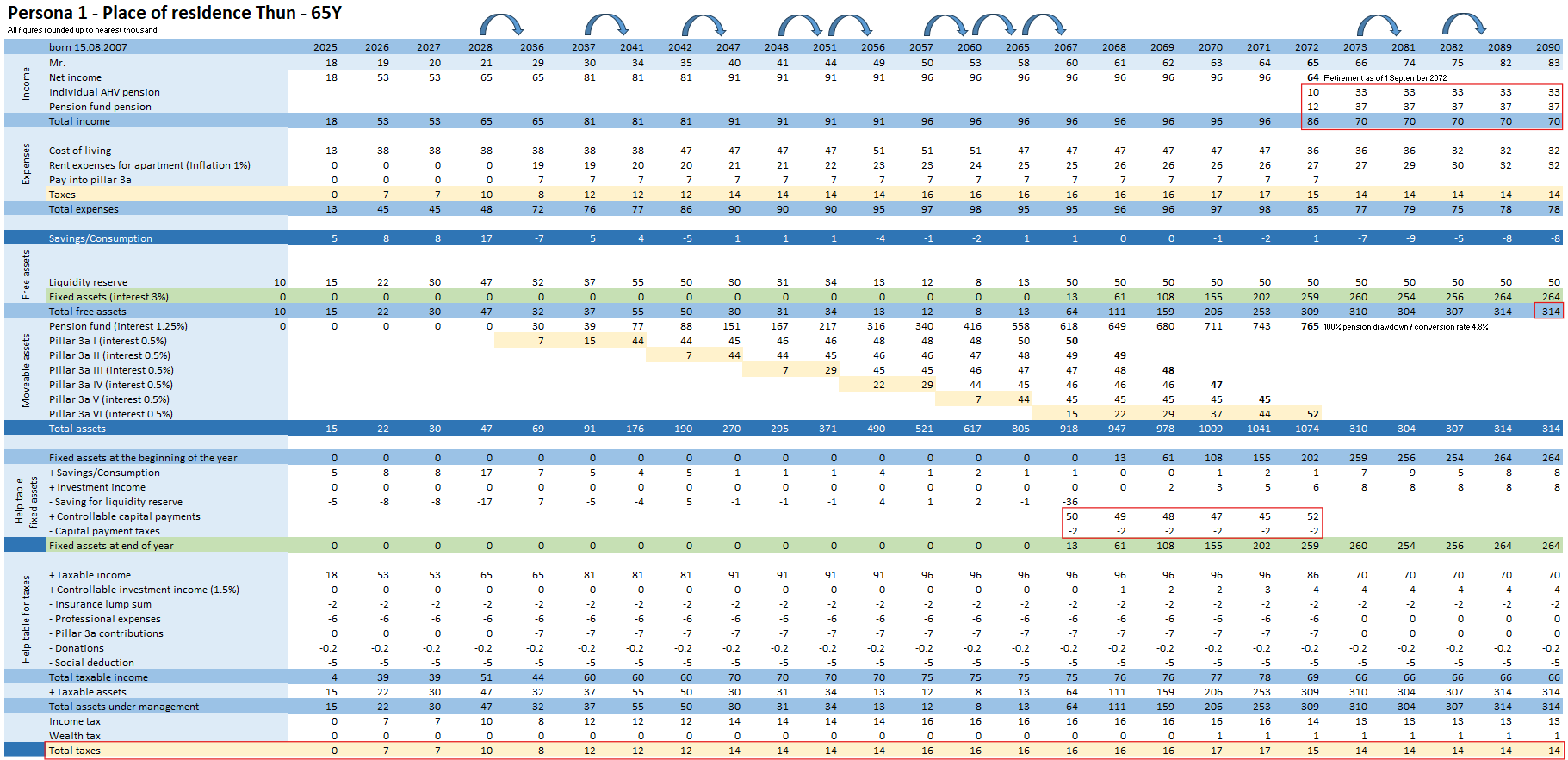

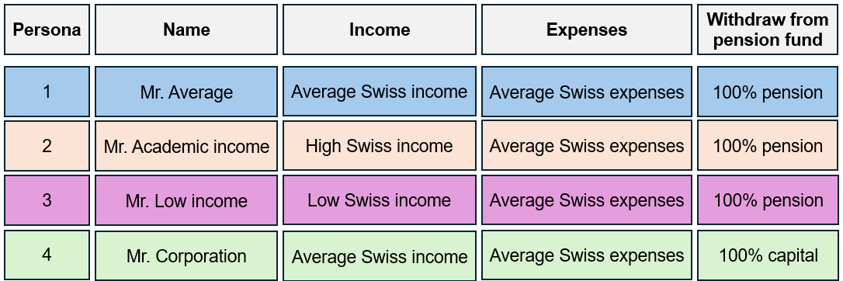

Four personas were developed to illustrate the financial implications. The personas all have the same expenses and differ only in terms of their income and pension fund benefits (pension/capital). Four retirement scenarios were calculated for each persona and then compared with each other. Finally, sensitivity analyses were carried out to weigh up the risks. These examined the risks of longer life expectancy, higher expenses and lower returns. In addition, it was examined when it makes sense to draw a pension or withdraw capital from the pension fund.

Empirical analysis and evaluation

Pension income is significantly lower in the event of early retirement. The analysis shows how important the final years of working life are for building up pension assets. As long as there are still free assets available at the end of the planning horizon, retirement is financially viable. In the event of early retirement, assets are used up more quickly due to the income gap and lower pensions. Pillar 3a is reduced in the event of early retirement, as no further payments can be made after the end of employment. The only positive aspect is that the tax burden is reduced due to lower income and assets.

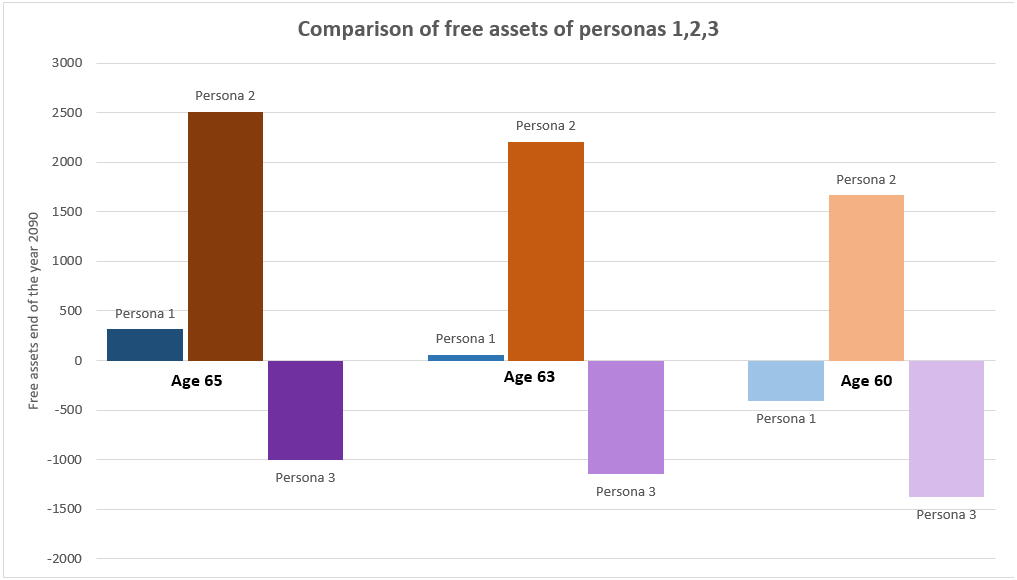

The study shows that higher earners can afford early retirement more easily. A higher income also means higher pension payments. The analysis shows that persona 2 with a high income can easily afford early retirement, while persona 3 with a low income cannot even afford a decent retirement.

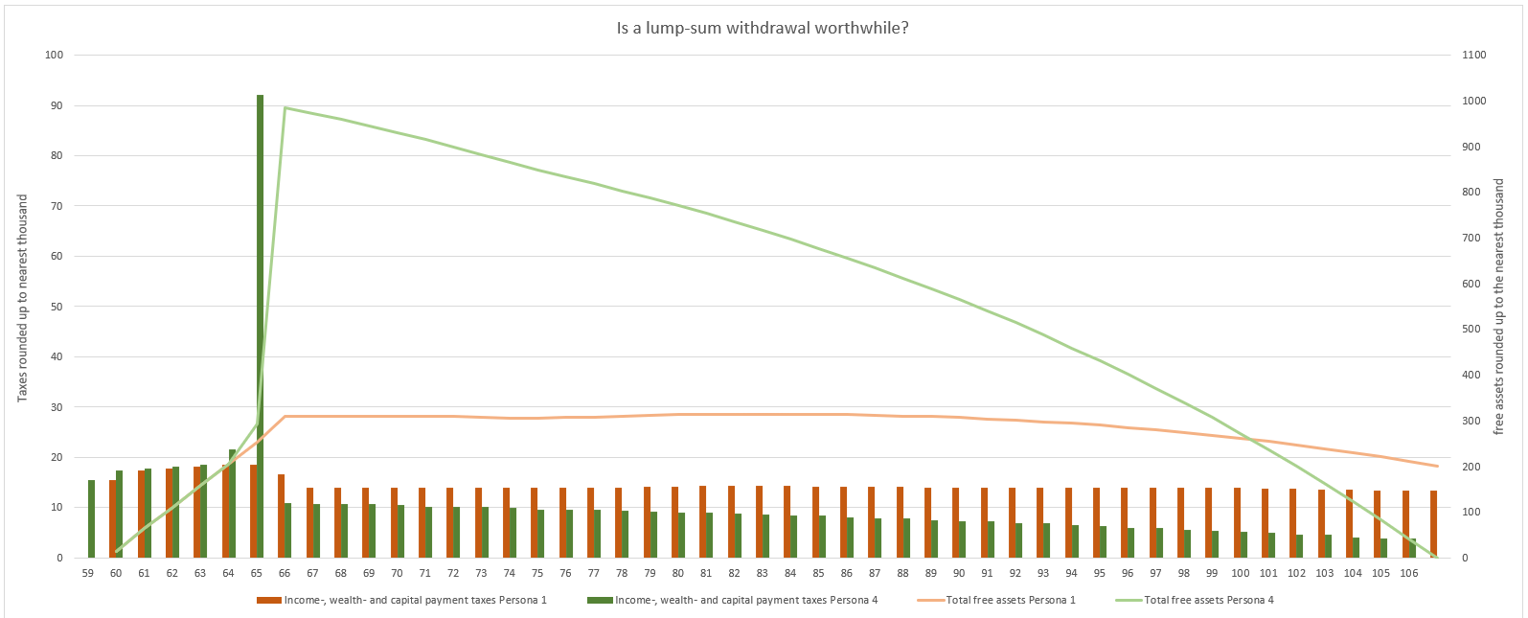

The analysis showed for personas 1 and 4 that a pension or lump-sum withdrawal depends on life expectancy and the expected return. A lump-sum withdrawal tends to make more sense in the case of early retirement, as you are not penalised by the lower conversion rate. In summary, a pension means high taxes but security after retirement, while a lump-sum withdrawal means flexibility but risky fluctuations in returns.

In summary, early retirement reduces both pension income and long-term financial stability. It is only financially viable for people with sufficient savings, careful tax and investment planning, and low fixed costs. Early retirement is a privilege and requires long-term individual planning.